Marcus & Millichap’s July 2026 Economic Outlook points to strengthening economic momentum that could bolster commercial real estate demand in the second half of the year. After a sluggish stretch that saw nearly 50,000 jobs lost between May 2025 and February 2026, the labor market has rebounded, adding roughly 550,000 positions since March. The report notes that sustained hiring and unemployment in the low-4% range would particularly benefit apartment and office sectors.

Labor market rebound points to optimism.

- The U.S. economy faced significant headwinds over the past 15 months, including tariffs, weak job creation, and geopolitical disruptions, all of which contributed to inflationary pressures.

- Despite this, overall economic performance has remained durable, signaling underlying resilience across key sectors.

- From May 2025 through February 2026, labor market conditions weakened, with a cumulative loss of nearly 50,000 jobs and reduced workforce mobility.

- Hiring activity shifted notably beginning in March 2026, with approximately 550,000 jobs added over the last four months, indicating renewed labor market momentum.

- Job growth has been concentrated in major metros—including New York, Dallas, Phoenix, Orlando, Los Angeles, and Houston—reinforcing demand for space across key CRE markets.

- If sustained, ongoing hiring and stable unemployment in the low-4 percent range would support CRE demand, particularly in apartments and office spaces.

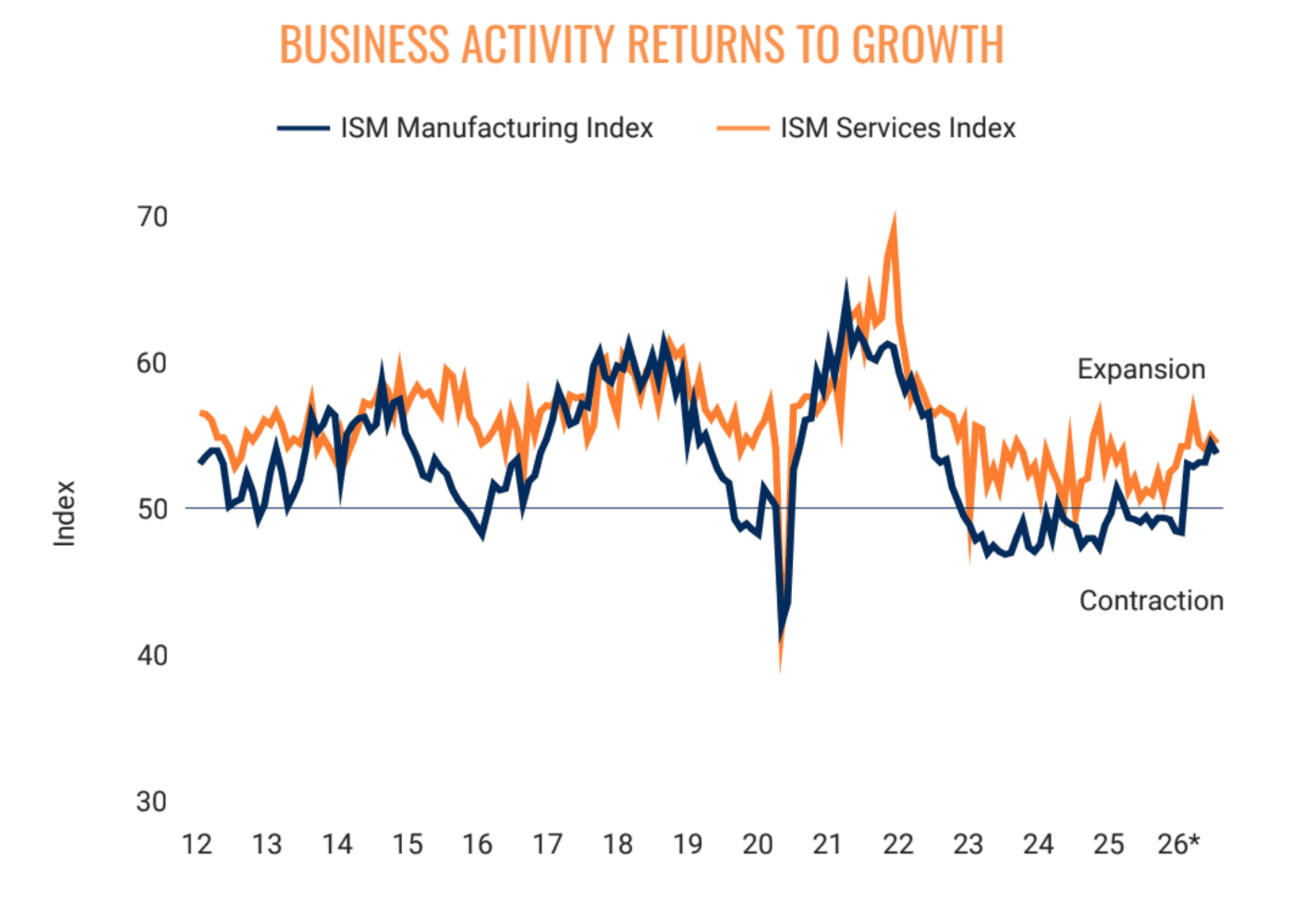

Business activity expands.

- Indexes from the Institute for Supply Management (ISM) Manufacturing and Services are signaling renewed economic expansion following a period of stagnation.

- The Manufacturing Index, which remained in contraction territory for much of the last year, has moved above 50 since January, indicating growth is returning.

- The Services Index has also strengthened, rising from near-break-even levels to the mid-50s, signaling steady expansion across the 15-plus industries it tracks.

- ISM indicators have historically served as reliable signals of broader economic cycles.

- Continued momentum in these indexes supports a positive outlook for demand in industrial and retail real estate.

Consumption strength meets economic risks.

- Retail sales have emerged as a key pillar of economic resilience, with headline sales rising 6.9 percent year-over-year in May and core sales up 5.6 percent.

- On an inflation-adjusted basis, core retail sales increased 2.2 percent, indicating real growth in consumer spending.

- Despite concerns about elevated consumer debt levels, household debt service remains manageable at 11.2 percent of disposable income, 60 basis points below the pre-pandemic average for 2012-2019.

- Continued growth in retail sales supports sustained demand for retail and industrial CRE.

- Several risks remain, however, including ongoing tariff pressures and uncertainty surrounding the renegotiation of the United States-Mexico-Canada Agreement.

- Geopolitical instability, including a fluid situation in the Middle East, and an uncertain inflation outlook continue to pose potential challenges to sustained economic expansion.

- Financial markets are currently anticipating a 25-50 basis point interest rate increase by year-end, though easing inflation could reduce pressure on the Federal Reserve.

- Even with lingering headwinds, stable or modestly declining interest rates would support a favorable investment environment and reinforce improving CRE demand.